The Federal Reserve underwent a massive regime shift following the 2008 financial crisis. It incorporated several new tools into its monetary policy arsenal, ranging from interest on excess reserves to large‐scale asset purchases (“quantitative easing”) to deal with the crisis. Unfortunately, as with most public institutions, power given is seldom relinquished.

As a recent Cato CMFA article noted, if the Fed is expected to massively increase its balance sheet in response to every major crisis, it will never return to a pre‐2008 operating system. Furthermore, the COVID-19 pandemic spurred a further round of massive quantitative easing, so much so that instead of shrinking back down, the Fed’s asset holdings are now over one‐third the size of the entire US commercial banking sector.

It stands to reason that such a massive shift in central banking should have effects on the financial system. A recent Wall Street Journal opinion piece makes this argument and uses options market data to suggest that the Fed’s involvement in financial markets has increased stock market volatility.

To be fair, the article points out a singular observation, one which may not reflect any underlying trend.

But there are ways to check for any underlying trend, such as vector autoregressions (VARs). In this post, I use a VAR method and demonstrate that the Fed’s 2008 regime shift has indeed had serious repercussions for market volatility as measured with the CBOE Volatility Index (“VIX”). (For those interested, I provide more details on the methodology after discussing the results.)

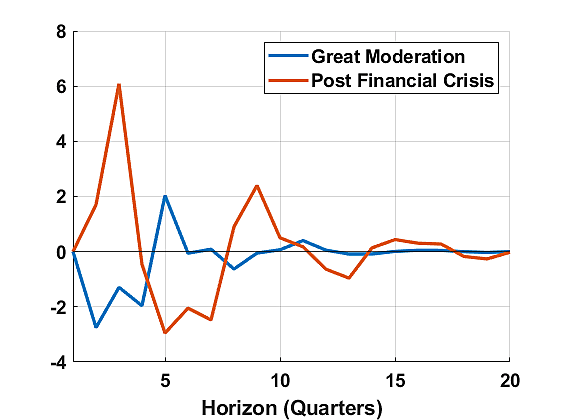

Figure 1 shows the response of the VIX to an unexpected one‐percent increase in Fed asset holdings. It is immediately clear that the relationship between the Fed’s balance sheet and volatility has flipped since 2008. Prior to the financial crisis (the blue line in Figure 1), when the Fed purchased more assets, market volatility slightly declined. A 1 percent increase in asset holdings reduced volatility by around 2 percent at peak efficacy. After the crisis (the red line in Figure 1), under the Fed’s quantitative easing framework, an increase in asset holdings significantly increased short‐term market volatility. In this period, a 1 percent increase in assets led to a 6 percent increase in volatility at peak efficacy.

And there’s more.

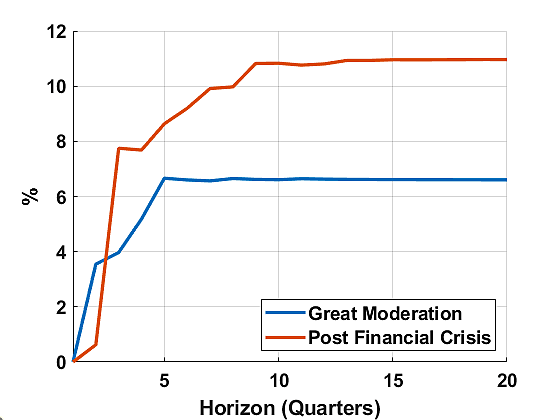

Figure 2 shows that the amount of market volatility that is attributable to Fed balance sheet shocks increased after the 2008 regime shift. Put simply, the percentage of all fluctuations in market volatility that is attributable to the Fed has increased. Prior to the financial crisis, the Fed accounted for around 6 percent of the fluctuations in the VIX. Following the crisis, it has accounted for well over 10 percent of the movements in the VIX. So, along with increasing the severity of market volatility fluctuations, the Fed has also become more responsible for overall market volatility post‐2008.

Though it is not shown in Figure 2, the portion of volatility now attributable to the Fed is similar to the degree by which overall demand and supply factors influence the VIX. That is, the Fed’s actions are now roughly as important in driving volatility as overall economic conditions.

There may be several possible explanations for this flip in the transmission of the Fed’s asset purchases to volatility under the new framework. Before the crisis, asset purchases were not in themselves considered a means of easing or tightening. Market participants may now view Fed asset changes as a signal of weakening economic conditions due to the scale and frequency of quantitative easing measures. Conversely, before 2008, balance sheet expansions were less common and typically viewed as a routine adjustment or a response to relatively minor financial disruptions. The nature of the assets being purchased also changed post‐2008, when the Fed, for the first time, expanded its asset purchases to include a large quantity of mortgage‐backed securities. And, of course, in response to COVID-19, the Fed also began purchasing corporate bonds and ETFs.

Once again, the empirical evidence supports reigning in the Fed; the economy works better when the Fed does less, not more.

For those interested, here is a brief description of the VAR method used for this post. A vector autoregression with four lags is fitted to quarterly data on four variables—output gap (i.e., how far US real GDP is away from its potential capacity), inflation computed using the GDP deflator, percentage change in the VIX, and percentage change in the Fed’s total asset holdings.[1] The VIX uses stock index option prices to measure the market’s expectation of short‐term volatility. Since the goal of this post is to compare the Fed’s effect on volatility under its post‐2008 operating framework, the VAR is estimated over two data samples—1991 through 2007 (“Great Moderation”) and 2009 through 2019 (“Post Financial Crisis”). The start year is set at 1991 to match the first full year when VIX data are available. The full year of 2008 is skipped to ignore the transition between the Fed’s pre‐crisis and post‐crisis operating framework.

The Fed’s framework has arguably changed again following the COVID-19 pandemic but there has been insufficient data since then to estimate any meaningful statistical model. Moreover, the Fed is still operating in an abundant reserve framework, and paying interest on reserves, both of which are the major defining characteristics of the new operating regime.

This VAR method offers important advantages when trying to empirically describe the relationship between the Fed’s balance sheet and volatility. Firstly, it includes macro indicators (output gap and inflation) so that any common changes in volatility or asset holdings resulting from responses to general economic conditions are not mistakenly attributed to each other. Secondly, such a method prevents obfuscation created through the cross‐dependence of volatility and assets on each other. That is, it will not incorrectly attribute the effects of volatility on balance sheet size in the other direction.

The author thanks Jerome Famularo and Nicholas Thielman for their invaluable research assistance in the preparation of this essay.

[1] All data is collected from the FRED database. Compiled Fed balance sheet data is only available directly from the Fed from late 2002. Bao et. al. (2018) extend this dataset all the way back to the Fed’s inception. Their dataset is used from 1991 until the start of the Fed’s own data series.